The Government Employee Pension Fund, budget austerity and the Eskom debt crisis

Dick Forslund |DailyMaverick

Finance Minister Mboweni announced a Special Appropriation Bill in August which added R59-billion over two years to Eskom. The government will now have even higher debt service costs.

There is an absurd aspect to this appropriation. Why is Mboweni not negotiating debt relief with a creditor that is in fact an organ of the state? The same irrationality applies to the February 2019 announcement that the Treasury allocated R69-billion from the national budget over three years to Eskom’s debt service.

It is in fact, arguably, also unconstitutional, given that government’s constitutional mandate is to gradually improve the lives of all “within its available resources”.

Is there another way?

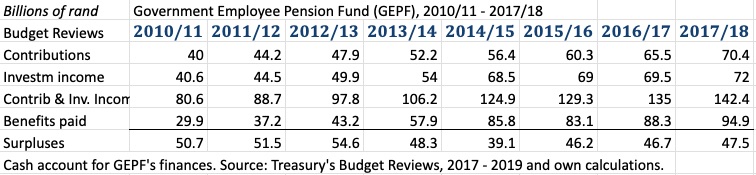

In the 2017/18 fiscal year, the government paid an estimated R25-billion in interest on its R359-billion debt to Government Employee Pension Fund (GEPF). The GEPF owned, at that point, 14% of the gross loan debt of the government.

Eskom’s debt to the GEPF in March 2018 was R87-billion. This was 20.8% of Eskom’s whole R419-billion debt in 2018. The GEPF probably earned a market rate interest of some R8-billion on this investment, because of Eskom’s low credit rating.

At least 45% of the GEPF’s R72-billion cash income from investments in 2017/18 came from the government itself and from the state-owned Eskom.

The crucial question is whether the R1,802-billion GEPF (as at March 2018) actually needs these income streams to pay government pensions and benefits to members at the guaranteed levels?

The Government Employee Pension Law of 1996 (GEP Law), requires the funds of GEPF to cover 90% of all liabilities at any point in time. The actuarial audit of GEPF concluded that on 31 March 2018, the GEPF had R1,802-billion in financial assets managed by PIC. It covered 108% of GEPF’s liabilities to working and retired members.

This means the market value of GEPF’s financial assets could have been R304-billion less in March 2018. It would still have met the 90% legal requirement. At a 100% funding of liabilities, which is the political goal of the board, the surplus was R137-billion.

Why does the law stipulate a mere 90% “funding level”? Mustn’t all pension obligations be paid?

They have to be paid, but not all of them on the same day.

The statutory audit controls if the market value of the fund’s financial assets on a certain day is enough to pay “the present value” of past and estimated future liabilities to those who are members on that day and until they die. If it is, then the scheme is 100% fully funded.

The “funded” pension scheme must have all the money in advance, like a well-paid but lonely individual who calculates how much she should save until she stops working and will start to withdraw money from an account until she dies.

In contrast, the so-called “Pay-as-you-go” pension system uses the fact that no pension scheme on a certain day has to pay all it owes and will owe to all its members. It works on the basis that every month, “My pension is, because others’ contributions are”. Pension liabilities are paid bit by bit over a time span of 30-50 years.

Before neo-liberal economic policies became dominant in the 1980s, pay-as-you-go was standard policy for state pension schemes in countries with strong labour movements. Surpluses build buffer funds as protection against shocks and financed investments in social infrastructure.

But no matter how it is constructed, no pension scheme is actually paying the theoretical “present value” of all present and future liabilities to those who are members on a certain day. In this world, it never requires that theoretical “100% coverage”.

This is why South Africa’s GEP Law can set the minimum to 90% funding “in advance” of liabilities and why, for example, the legal demand on the funding level of a private pension scheme in the US is put at 80%, or why the credit rating agencies Standard & Poor, or Fitch, only regard a funding level as “weak” if the funding level is below 60% in a public pension scheme like GEPF. The “underfunding” allowed for in the GEP Law is a kind of concession to the practical power of an “unfunded” pay-as-you-go scheme.

In the case of GEPF, the power of pay-as-you-go reality has been boosted with large cash flows from dividends and interests on investments. For fourteen years, investment cash flows were not touched to pay benefits. They were all reinvested by PIC. Contributions were equal to or higher than benefits paid from 1998 to 2013. The contribution surpluses were also invested. The result was exponential growth of GEPF’s financial assets, only interrupted by the stock market crash 2008-2009.

For this reason, finance ministers and GEPF boards have never followed the auditors’ recommendations to increase the employer contribution rate. The 2018 audit had the same recommendation, but the level stayed at 16% on salary for service staff and 13% for all others, giving an average of 13.5% in employer contribution. In many private pension schemes 7.5%, is the norm that is deducted from the salaries of the employees.

A generous rule change, from 1 April 2012, let members withdraw their whole “actuarial interest” share in the GEPF if they resigned before retirement day, instead of using a defined benefit formula for early resignations unrelated to developments in the capital markets.

The change led to mass resignations. This was encouraged by the finance industry: The lump sums should, of course, be moved to private schemes to attract hefty fees. An eyewitness tells us Finance Minister Pravin Gordhan pleaded with delegates at Fedusa’s 2013 wage bargaining conference to start a campaign for members not to leave the GEPF.

But benefits paid doubled from R43.2-billion in 2012/13 to R85.8-billion in 2014/15 (stabilising at that level). Also, a part of cash flow from dividends and interest incomes now had to be used to pay benefits from 2013/14, for the first time since 1998.

The incident demonstrated the healthy state of the fund even when hit by shocks, like unintended consequences of policy changes. The contribution rates stayed put. The GEPF’s cash income surplus in the 2018 fiscal year was R47.5-billion. There were no additional payments from the government to deal with the shock.

The big crisis in Eskom, and the huge impact Eskom’s collapse would have for all of us, requires serious consideration of alternatives. In time of debt crisis for governments, private creditors have often been offered a so-called “haircut” or stand the risk of losing all their claims.

A “haircut” can mean to get a lower interest on a loan. Any kind of more or less radical options exists. Alternatives can range from simply writing off the debts to delaying the payback. Converting ordinary bonds into “zero-coupon bonds” has been suggested by Magda Wierzycka: The loan, and the interest on it, is only paid when the loan period expires. But this only provides a short-term liquidity relief.

As it stands, GEPF can take a haircut of its R87-billion bond claim on Eskom with no risk for the guaranteed pension payments. It can forfeit some R8-billion in interest income from its Eskom bonds, converting the bonds to an interest-free loan. The Treasury’s instruction to departments before the Mid-Term Budget to cut spending by 16% over three years is what should alarm the public, the over one million public sector employees and their unions, including their representatives in the GEPF board.

Earlier this year, headlines claimed that GEPF had a “long-term funding shortfall” of R573-billion. The main reason for this actuarial shortfall is GEPF’s too risky investment policy. Over 50% of the funds are placed in equity. The solvency fund guards against financial crashes. It is only filled to a third. Also, this should compel a shift to government bonds, which should be bought at regulated interest rates.

Eskom is too big to fail, but the Treasury must stop supporting Eskom via the national budget, borrowing more money for this purpose at market rates and unnecessarily increasing its debt service costs. The political agenda must change. Austerity must be reversed, not sharpened.