Dick Forslund | BusinessLive

In August, the National Treasury issued a discussion document “Towards an economic strategy for SA”, asking for discussion. “Exports have been identified as a key driver of economic growth” was a priceless statement in the Treasury document, which means, “We agree!”

It was 15 authors of a document called “Growth, Employment and Redistribution” (GEAR) who, 23 years ago, put forward the “export-oriented strategy” that would “lay the basis for an export-led revival of the economy”.

To that end they argued for “further steps in the gradual relaxation of exchange controls” and asserted that “the general direction of economic policy is towards greater openness and competitiveness”, bravely admitting that “the economy will thus become increasingly subject to global forces”.

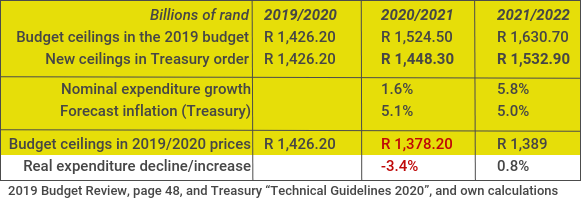

And so it evidently has. In July, the Treasury prepared for the medium-term budget policy statement (MTBPS) by directing all departments as follows: “A compulsory budget baseline reduction scenario of 5%t in 2020/2021; 6% in 2021/2022; and 7% in 2022/2023…”

If this goes ahead, public spending (excluding debt service) will be cut by about 3.4% in real terms in 2020, that is, after accounting for inflation.

Government spending comprises almost a third of GDP. If the budget ceiling (total public services and investment spending) is lowered by more than 3% in 20202, more than 1% will be cut from GDP. This will provoke a recession and increase mass unemployment. Alternatively, such a budget cut will tremendously deepen the effects in SA of a global recession that might already be on its way.

The notion, or spin-doctor jargon, that the Treasury has a plan to “kickstart growth” is absolute nonsense. The Treasury is heading for the opposite.

GEAR, where it all started

We put it to the Treasury that the immediate rationale for this extremist plan is found in the old GEAR document of 1996.

The commendably non-anonymous authors of GEAR wrote that “the balance of payments remains a structural barrier to accelerated growth”. This balance is about how much foreign currency a country has available in its bank system to continue to import goods and services, as well as to pay back loans taken in dollars and other “hard currencies”.

In 1996, the GEAR authors also wrote: “The economy is dependent on imported capital and intermediate goods … the lack of sustained long-term capital inflows has made the balance of payments and the economy too reliant on short-term reversible flows and consequently high interest rates.”

Another recession … will cut imports even more than a simple business cycle downturn. It will save more dollars, guarding against possible outflow shocks and a payment crisis

Today, tools, machines and advanced equipment continue even more to be bought for hard currency because of de-industrialisation. There is even less inflow of capital for long-term investments. But there are huge foreign currency outflows of dividends from profits and payments to foreign lenders, as well as billions in illicit hard currency outflows. Unfortunately, the export-led trade and capital markets liberalisation policy of GEAR made unemployment and the unacceptable situation in 1996 worse.

The “structural barrier” the GEAR authors spoke of is like this: the SA Reserve Bank cannot allow a payment crisis. It sets interest rates high so that foreign investors will prefer SA bonds, but they must change their money to rand before buying financial assets in SA. Their constant deposits of hard currency in the banking system make it possible to continue imports and payments of foreign loans. One problem is then solved — but the world record high interest rates in SA put a brake on economic growth.

In “the short term” that must not matter. An economic downturn and slow growth in general save foreign currency in the vaults of the banks and the Reserve Bank: the export-led liberalisation strategy has failed and has been taken over by an approach that doesn’t question dogma.

This is why, during the Alternative Information and Development Centre’s (AIDC) recent conference on illicit financial flows, Prof Seeraj Mohamed asked whether the Treasury doesn’t mind another recession. It will cut imports even more than a simple business cycle downturn. It will save more dollars, guarding against possible outflow shocks and a payment crisis.

But what does this extreme austerity policy and “import compression” lead to?

Turn to local funds

We have, in other articles, suggested that the government stop using the public service delivery budget and tax money for Eskom and other state-owned enterprises (SOEs), which owe 45% of their debts to foreign investors. It must turn to the local funds under its control.

The Public Investment Corporation (PIC) handles more than R2.1-trillion in funds, largely deposited there by the Government Employee Pension Fund (GEPF) and the Unemployment Insurance Fund (UIF). These funds can be used for regulated borrowing to the government without any threat to pension benefits. GEPF runs a surplus of R50bn per year. The UIF has accumulated a staggering R170bn, for no good reason.

But in response to the extreme mid-term budget plans, so-called “capital controls” must also be considered. Argentina has recently introduced capital controls to stop a payment crisis. This is what GEAR opposed 23 years ago, in a policy document that made some correct observations, promised wonders — but contributed to the present social disaster.

Will capital controls lead to a credit downgrade? The Treasury has used the threat of a credit downgrade for too long. Let’s consider it inevitable, if not in November then early in 2020, because of an extremist budget also affecting tax revenue, or triggered by any local or global event. Under a regime of liberalised finance, a downgrade will indeed lead to a sudden financial outflow of international pension fund investments and maybe even a shortage of foreign currency.

Instead of wasting the downgrade on Treasury’s recession budget and whatever economic policy agenda that will surface in the increased social chaos, it is better to cash in that downgrade for a good purpose, which contains its effects and regains some independence. This is what the Treasury cannot and will not discuss: a complete overhaul of economic policy.

• Forslund is senior economist at the Alternative Information and Development Centre.